-

5. External vulnerability mitigation instruments (FFAR, FECR, IFR)

-

7. Capital buffers of systematically important institutions (OSII-B)

-

11. Financial stability risks of climate risk and options for their macroprudential management

-

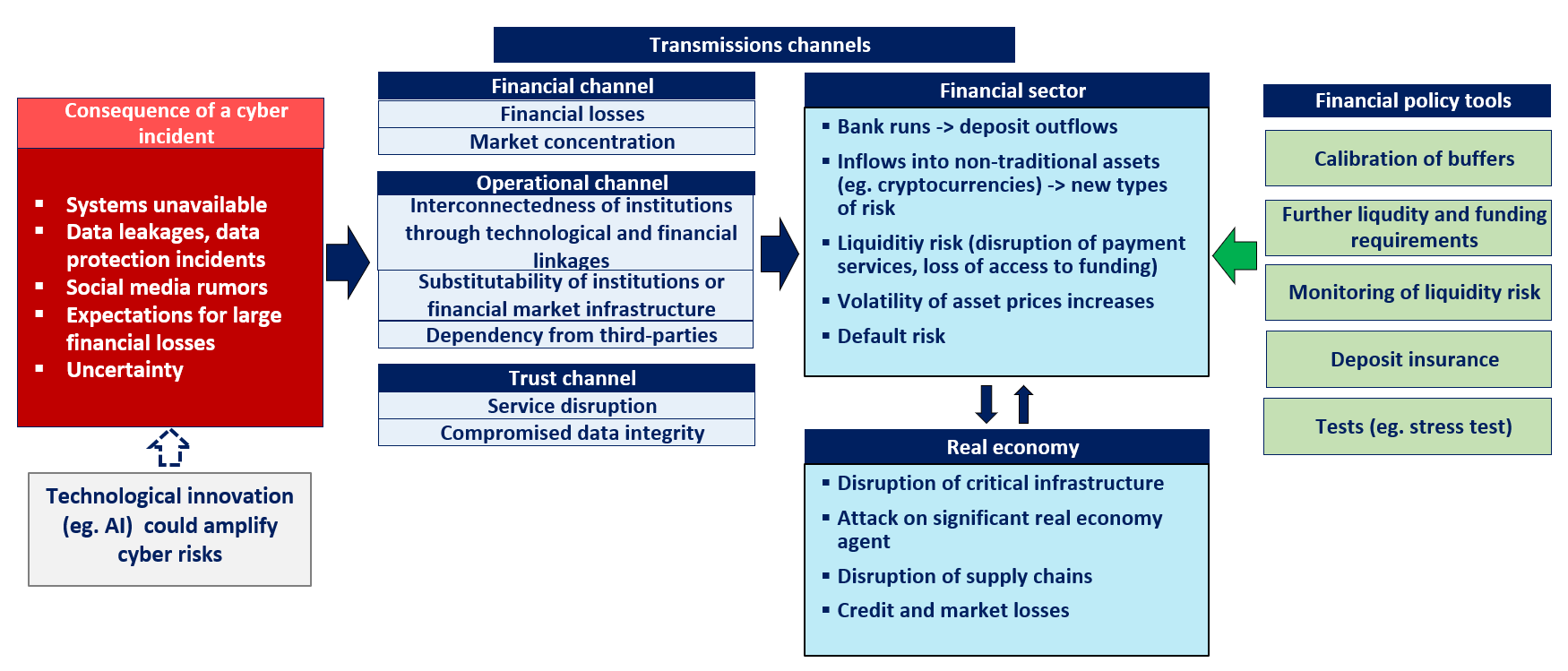

13. Focus: Financial stability implications of the turn in the financial cycle

1. Executive summary

2. Countercyclical capital buffer (CCyB)

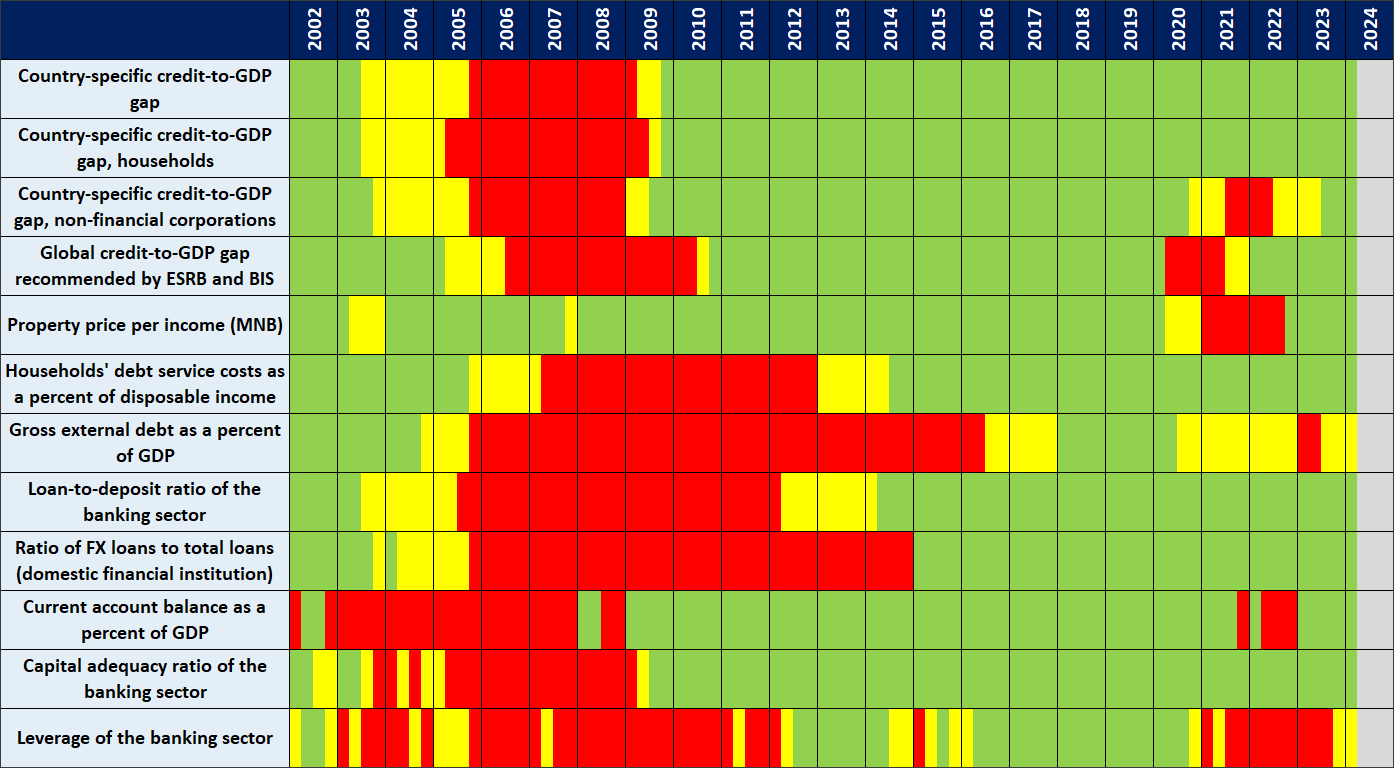

2.1. Cyclical systemic risks have continued to decline over the past year

Based on the country-specific benchmark additional credit-to-GDP gap as a starting point for the rule-based assessment of the domestic credit cycle, the risk of overheated lending is steadily declining since the beginning of 2022. The additional credit-to-GDP gap for the household segment shows a credit-to-GDP ratio that has been consistently below the estimated equilibrium level since 2010. In the corporate segment, the indicator points to a declining credit-to-GDP since the beginning of 2022, indicating a close-to equilibrium level by the end of 2023 (Figure 1). Looking ahead, as the macroeconomic environment improves and lending grows, the benchmark credit gap is likely to gradually narrow.

Chart 1: The evolution of the benchmark additional credit-to-GDP gap

Source: MNB

The indicators of the cyclical systemic risk map, which measures cyclical systemic risk, also indicated a decline in cyclical risks over the past year. At the end of 2022, gap indicators referring to corporate lending showed a medium risk and external balance indicators showed elevated or high risk due to the Russo-Ukrainian war and the subsequent inflation shock. However, as inflation shocks phase out and lending slows down, these indicators already point to a medium risk with declining dynamics by the first quarter of 2024 (Chart 2). Therefore, the level of domestic cyclical financial systemic risks does not require macroprudential intervention, either on a rule-based basis or according to the quantitative and qualitative information monitored.

Chart 2: The cyclical systemic risk map (Q1 2024)

Source: MNB

2.2. In EEA countries, CCYB is being raised along with enhancing banks’ resilience

In view of the intensifying financial stability risks, macroprudential capital buffers are being increased in most EEA countries, but there are still countries that do not apply such buffers. According to the assessment of the European Systemic Risk Board (ESRB), the macroeconomic environment in the EEA is improving, but the risk of unforeseen shocks remains significant due to geopolitical tensions and uncertainty. Accordingly, 22 EEA countries have already reported positive CCyB ratios by the end of June 2024 to strengthen the banks’ resilience to shocks. In 8 EEA countries, the CCyB requirement is still at 0 percent, but all countries in the CEE region have already set a positive CCyB requirement (Chart 3). Countries that did not activate the CCyB requirement opted to maintain the 0 per cent rate mainly because of declining cyclical risks and negative credit-to-GDP ratios.

Chart 3: CCyB requirements in the EEA countries (July 2024)

Note: Buffers announced but not necessarily activated. The CCyB rates shown relate to the exposures of the relevant country. *Countries using or planning to implement a framework that can be considered as a positive neutral CCyB rate. Source: ESRB, websites of national authorities. Source: MNB

In the EEA countries, the so-called positive neutral application of the capital buffer, independent of the increase in cyclical risks, is also becoming increasingly common (Positive Neutral Rate of CCyB, PNR CCyB). In this case, the CCyB rate to be used is a combination of a cyclical CCyB rate, which is dependent on the overheating risk, and a so-called positive neutral rate of CCyB, which is determined in a ”normal” risk environment, i.e. also in a period without cyclical overheating risks. A positive neutral rate of CCyB is thus not only aimed at addressing the cyclical systemic risks that characterise the overall operation of the financial system, but also support the macroprudential counterbalancing of a potential macroeconomic shock. The aim of a positive neutral ratio of CCyB is therefore to ensure that authorities have sufficient capital buffers available to be released in the event of unforeseen shocks from outside the financial system, such as the coronavirus pandemic or the Russo-Ukrainian war.

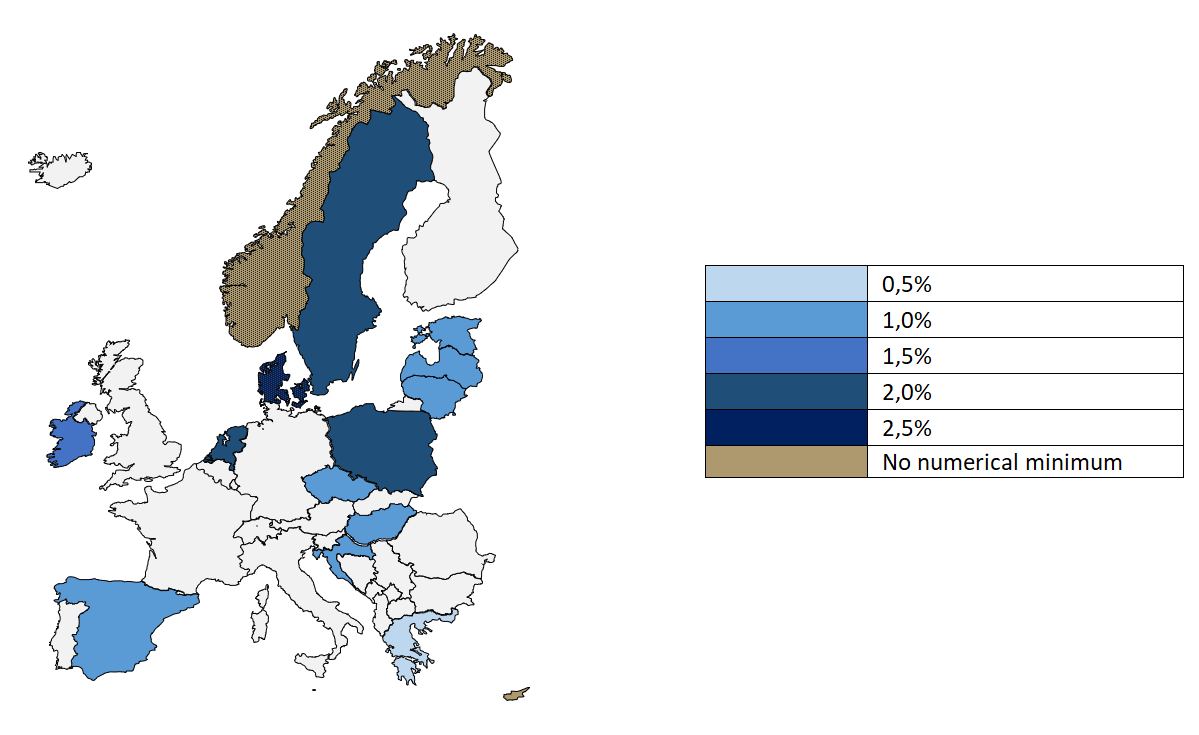

Currently, 15 EEA countries apply a positive neutral or similar so called early-build-up CCyB framework, with 0.5 to 2.5 per cent, but in our region most often with 1 per cent positive neutral CCyB-rates (Chart 4). In the CEE region, the Baltic States, the Czech Republic and Slovenia have a positive neutral CCyB rate of 1 per cent, Poland 2 per cent, while the Nordic countries have higher rates of 2–2.5 per cent.

Chart 4: Applied positive neutral CCyB rates in the EEA countries (July 2024)

Note: Countries using or planning to use positive neutral CCyB or an ”early CCyB build-up“ similar to positive neutral CCyB (indicated by the pattern filling in the map). In Norway, authorities are targeting the upper half of the CCyB rate range of 0–2.5 per cent, without setting a numerical minimum. In Cyprus, the target is a CCyB rate above 0.5 per cent, but no numerical minimum rate has been set. Source: ESRB, websites of national authorities.

2.3. To further strengthen the resilience of banks to shocks, the MNB decided to apply the positive neutral CCYB framework in Hungary

In its June 2022 rate review, the MNB decided to activate the CCyB rate applicable to domestic exposures at a level of 0.5 per cent. In view of the easing of cyclical systemic risks and the risks associated with the overvaluation of the housing market, it was postponed by one year at the June 2023 rate review to 1 July 2024.

In June 2024, the MNB decided to implement the positive neutral CCyB framework in Hungary as part of its review of the strategy and methodology for the application of the CCyB. Domestic cyclical systemic risks have remained low over the past year as lending activity has declined. However, the level of geopolitical and macroeconomic uncertainty remains high, calling attention to the importance of maintaining a strong banking system capital position and of building-up capital buffers. In addition, the current record level of bank profitability will allow credit institutions to accumulate capital more intensively. Against this background, and also in the light of the recommendations of international institutions on the build-up of capital buffers, the MNB, following the extending European practice, decided on the domestic application of the positive neutral CCyB framework and, accordingly, on the renewal of the CCyB strategy and methodology.

Under the new framework, a positive neutral rate of 1 per cent has been set for a neutral risk environment that is not yet characterised by excessive cyclical risk. The requirement will enter into force on 1 July 2025 and will be a minimum requirement in future non-crisis periods. The MNB may set a requirement of over 1 per cent depending on the evolution of cyclical systemic risks in its quarterly rate decisions, with the higher of the rate reflecting cyclical systemic risks and the positive neutral rate of CCyB of 1 per cent becoming applicable (Chart 5). In the event of a stress situation, the MNB will decide on the need to release the entire required capital buffer. The introduction of the new framework will therefore allow the banking sector to hold a capital buffer in non-crisis periods of at least 1 per cent of the domestic risk exposure value that can be released in a crisis situation, regardless of the state of the financial cycle.

Chart 5: The operation of the Hungarian CCyB framework

Source: MNB

Given the current strong capital position of banks, imposing a higher capital buffer would not impair the lending capacity of institutions and would not lead to a significant increase in interest rates. Based on the capital position as of 30 June 2024 and considering the imposition of the CCyB at the level of 1 per cent as from 1 July 2025, and assuming that all other factors remain unchanged and considering the uncapitalised interim profits, banks have a HUF 2,157 billion of free capital at their disposal at sector level (Chart 6). The total use of this could allow for the disbursement of household and corporate loans in the amount of around HUF 26,000 billion, assuming that the household and corporate exposure ratio and average risk weight of individual banks are fixed, and that the TREA increase could be achieved by using the free buffer. Based on this, bank resilience can be strengthened by increasing the capital buffer requirement without any current negative lending effects. In addition, even in the case of an actual capital injection, the increase in the capital buffer would not lead to a material increase in costs for banks, and thus would not lead to a material increase in interest rates. The interest rate increase of a 1 per cent PNR CCyB requirement for a mortgage loan with a 35 per cent risk weight and a 12 per cent cost of capital could be in the order of 0.04 per cent on average.

Chart 6: Development of macroprudential capital requirements and the capital position

Note: Estimation focusing only on the change in the combined buffers, disregarding other additional regulatory capital requirements affecting the free buffers (e.g. possible change in Pillar 2 capital, P2G, etc.) and the MREL requirement, as well as the expected change in lending and profitability. Profit not taken into account: part of the mid-year or year-end profit that cannot be taken into account. Source: MNB

BOX 1: Development and new methods of using the cyclical systemic risk map

The MNB has started a multi-dimensional review of the cyclical systemic risk map supporting the regulation, based on its experience gained from almost a decade of CCyB implementation:

- Risk coverage: In order to cover the various cyclical systemic risks as comprehensively as possible, the current set of indicators will be developed and expanded, which would increase the total number of indicators in the map from 33 to 59.

- Structure: To improve transparency and easier comprehension, the monitored indicators are grouped into four major and several minor sub-groups according to the main task of the banking system and the individual aspects of lending: (1) credit institutions, (2) debtors, (3) collateral and (4) foreign countries.

- Balance: The monitored indicators are based on the segments that determine the evolution of cyclical systemic risks. Given that the evolution of Hungarian cyclical systemic risks depends on the characteristics of (1) lenders and (2) borrowers, these groups also account for the vast majority of the new indicators.

- Data availability: The use of several new indicators was made possible by the availability of new data sources. Examples include indicators related to overvaluation risks using commercial real estate returns, interest rate spreads based on specific HITREG data, or an indicator based on NSFR data available from 2021. Occasionally, more precise indicators with the same content have been developed, a typical example being the overvaluation rate indicator developed by the MNB and since then being used as a standard.

The evolution of indicators of the revised cyclical systemic risk map (2000- Q1 2024)

Note: The indicators are standardised based on their historical values, therefore the distribution of their deviation from their historical average, measured in units of historical standard deviation, is shown in the figure. 10th and 90th percentile, median and interquartile range values. The original values of indicators with lower values indicating higher risk were multiplied by -1. The only indicator with both low and high values indicating high risk has been omitted from the figure. Source: MNB

The indicator values are further divided into a range of low, medium and high cyclical systemic risks. In setting the risk thresholds, we rely heavily on values used in other countries or international organisations, as well as on expert estimates to take country-specific factors into account more efficiently. The adequacy of the set of indicators and thresholds is regularly reviewed and corrected as necessary.

The compilation of a validated set of indicators collected during the map review, which are highly correlated with cyclical risks, could also serve as a basis for several further methodological developments. The significant increase in the number of indicators associated with the map review makes it necessary to condense the information contained in the map indicators into a few aggregate variables. By significantly improving the ESRB/ECB methodology (Lang et al., 2019), we are planning to develop aggregate indices (Bondell et al., 2010; Jiang et al., 2014; Szendrei and Varga, 2023). This will allow the development of aggregate indices capturing the extent of cyclical systemic risks in a single indicator, which can be broken down and communicated according to their determinants, and even used as a leading indicator for CCyB determination.

The so-called anomaly detection method is able to identify events (e.g. the 2008/09 global economic crisis, the coronavirus pandemic or the outbreak of the Russo-Ukrainian war) that are not typical of the underlying dynamics of the map variables and that, once they occur, significantly change the risk level of the financial system. The method provides the possibility to estimate the probabilities of occurrence, the time of possible occurrence and the impact on the financial system, thus contributing to the early warning of financial stress situations, thereby supporting the CCyB’s resolution decisions. In addition, the procedure allows the assignment of an anomaly weight to each indicator of the map at each point in time, which can be used to refine the thresholds for the risk classification of the indicator values.

Among the methodologies for measuring systemic risk measures, Growth-at-Risk (GaR) models have become increasingly common in central bank applications since their introduction in 2017. GaR-type growth measures, as a supplement to the ”most likely“ growth projections, show the extent to which the magnitude of financial systemic risks could threaten the expected economic growth path. The basic tool of the GaR model is a so-called quantile regression procedure, which estimates the conditional distribution of future GDP reflecting financial risks by adjusting an estimate to each of the quantiles of the distribution.

The MNB’s GAR model can estimate medium-term growth risks depending on the actual financial situation. The model that has been commonly used by the ESRB (ESRB, 2021; ESRB, 2024) and the central banks (Adrian et al., 2019) to measure growth risks since 2016 has been adapted and further developed for Hungarian data. The set of variables in the model consists of the explained real GDP growth, the financial stress index included in the explanatory variables (Szendrei and Varga, 2017), and the optimally selected indicators and headline indices. The method is therefore suitable for quantifying the extent to which cyclical systemic risks in the financial system threaten to cause a crisis with severe real economic losses for 1, 4 and 8 quarters ahead.

3. Borrower-based measures

3.1. Household over-indebtedness remains invisible even with renewed growth in household lending

In the first half of 2024, a strong recovery in household lending activity, which was depressed by the inflation shock, can be witnessed. In 2024 H1, banks provided HUF 1,240 billion in retail loans, which is nominally the same as in 2021 H1, before the inflation shock (Chart 7). Regarding household mortgage lending, although still below the record levels of 2022 before the inflation shock, the growth rate of lending in 2024 H1 was particularly strong compared to the same period of the previous year, reaching an increase of around 150 per cent. The strong growth is explained by the normalisation of the interest rate environment and macroeconomic outlook, the materialisation of deferred loan demand, the increase in average loan amounts and the low base of the previous year. Regarding consumer credits, lending growth remained moderate, rising 34 per cent in 2024 H1 compared to the same period of the previous year.

Chart 7: The development of new household lending by loan type

Note: Credit institution sector. Without individual entrepreneurial loans. Source: MNB

Apart from the technical effect of the state-subsidised CSOK+ schemes, fixed-rate loans continue to dominate new mortgage lending for housing. The weight of floating rate home loan products in new loan disbursements has been negligible due to the impact of a number of MNB measures since the end of 2018, the increase in early 2024 being explained by the pricing methodology of the interest rate subsidy for CSOK+ loan schemes, which does not impose any real interest rate risk to borrowers (Chart 8). The cessation of new variable-rate loan products has also greatly accelerated the amortisation of the remaining portfolio, reducing the share of variable, non-subsidised interest rate mortgages in the total bank mortgage portfolio to 13 per cent by 2024 Q2.

Chart 8: The development of new residential mortgage lending according to interest rate fixing

Note: Loans from credit institutions, without individual entrepreneurial loans. Source: MNB

The share of housing loans with a high income burden is on the decrease with the normalisation of the interest rate environment, but the burden of collateral increases. The volume of household loans, which is clustered around the debt-service-to-income ratio (DSTI) limits, is gradually declining as the interest rate environment eases, especially in the case of housing loans. While in 2023, banks disbursed almost 33 per cent of housing loans at a high DSTI of over 40 per cent, this fell slightly to 32 per cent by the end of 2024 H1. The decreasing level of DSTI exposure on a volume basis may be explained by the increase in lending at lower DSTIs, which is confirmed by the fact that the DSTI distribution by number of contracts does not show a significant change compared to the trend of recent years (Chart 9). In terms of collateralisation, the weight of housing loans with a low down payment, or a loan-to-value ratio (LTV) of more than 70 per cent in new loan disbursements increased to 32 per cent by 2024 H1, compared to an average of 24 per cent in 2023. The increase in the collateral encumbrance can be explained by the decreasing income burden induced by the normalisation of the interest rate environment, the rising house prices, the growth of credit-financed home purchases, the reduction in non-refundable state subsidies, the shift towards interest-rate subsidised schemes, and to a lesser extent the more favourable LTV limit for first-time home buyers introduced in January 2024. However, the currently visible LTV values correspond to the level preceding the inflation shock, so the increase in the collateral stretch indicates a renewed strengthening in lending and does not point to a significant increase in risk exposure.

Chart 9: The development of new residential mortgage lending near borrower-based measures limits based on the number of contracts

Note: Overlap is possible between loans granted with a DSTI above 40% or with an LTV above 70%. The most typical effective DSTI and LTV limits. Source: MNB

Online lending is gaining ground. Full online lending is more common for uncovered loans, mainly personal loans, commodity loans and, to a lesser extent, prenatal support loans. In 2024, the share of fully online loans increased significantly, from 18 per cent in 2023 Q4 to 32 per cent in 2024 H1. This is mainly due to the increase in fully online, often pre-approved, personal loan disbursement, where the share rose from 29 per cent to 41 per cent. The increase in demand resulting from the growth in the availability of personal loans online may also have contributed to a smaller decline in the personal loan market compared to the housing loan market over the past year and a half.

Table 1: Main attributes of personal loans granted online and traditionally (2024Q1-Q2)

| Not or partially online administration | Entirely online lending | |

| Average loan amount (M HUF) | 2,7 | 2,4 |

| Average maturity (years) | 6 | 5 |

| Average APR (%) | 19 | 23 |

| Average DSTI income (K HUF) | 428 | 448 |

| Average DSTI (%) | 30 | 30 |

| Average age (years) | 44 | 40 |

Note: Credit institution sector. Source: MNB

There is no evidence of the excessive accumulation of risks in the case of online lending. In 2024 H1, the average maturity of fully online personal loans was 5 years, one year shorter than that of traditional loans. The average APRC for online loans is 23 per cent, which is 4 percentage points higher than for loans that are not fully online, probably due to the smaller amounts and a shorter maturity (Table 1). There is no significant difference between the two types of loans in terms of average loan amount, income and DSTI, therefore online loans do not pose a higher risk but can increase bank efficiency. There are no significant differences between settlement types of borrowers’ residence in the share of personal loans disbursed online.

Overall, household lending has a healthy structure, complying with the borrower-based measures, denominated in forints, with interest rates fixed over a longer period. The income and collateral stretch of borrowers do not indicate any signs of over-indebtedness.

3.2. The MNB supports the access of young first-time home buyers to mortgage loans by setting a more favourable LTV limit for them without excessively increasing risks

The MNB has introduced a higher 90 per cent loan-to-value (LTV) limit for first-time home buyers as from 1 January 2024, which is now applied by the majority of major housing loan providers. The share of loans with LTV limits above 80 per cent still accounted for only 2.6 per cent of all residential mortgage lending in 2024 H1, compared to the 12 per cent within borrowers who had claimed to be first-time home buyers and are eligible to higher LTV limits. The share of loans with LTVs between 80–90 per cent increased gradually over the six-months period, accounting for more than 4 per cent of total monthly lending by volume in June. However, higher LTV limits for first-time home buyers are also likely to have increased the amount taken by borrowers for higher but below 90 per cent LTV housing loans due to the often lower internal limits applied by institutions compared to regulatory limits. This is confirmed by the fact that the share of loans with 70–80 per cent LTV that do not directly utilise first-time home buyer limits also increased by about 6 percentage points compared to the previous year (Chart 10), while the LTV distribution did not change significantly for loans with lower collateralisation. Also for first-time home buyers, the share of housing loans with an LTV of between 70–80 per cent increased by nearly 6 percentage points compared to the previous year. At the same time, housing loans with higher LTVs are not coupled with higher DSTI, so borrowers are not considered to be under a tight income squeeze, and consequently, given the limited volume of total residential mortgage lending and the expected lower credit risk of the affected customers, the more favourable first-time home buyer limit introduced does not entail excessive systemic risk.

Chart 10: LTV distribution of new mortgage lending placements by volume*

Source: MNB

Based on data from the first half of the year, the first-time home buyer LTV requirement could have been a significant support for young borrowers with low down payment, but having sufficient income to achieve their housing goals. Based on 2024 H1 housing loan data, middle-income households account for the majority of first-time home buyer LTV limit users (Chart 11, left panel, share of HUF 600–900,000), and there is no significant strain in the distribution of these borrowers by DSTI, as the share of high DSTI borrowers did not increase even with the higher LTV limit (Chart 11, right panel). Among first-time home buyers, there is a higher share of those with no previous loans (either housing or other), and therefore their income squeeze is lower, which contributes to the lower DSTI level. In addition, there is no significant difference in the territorial distribution between the different types of settlements, therefore the higher LTV limit supports first-time home buyers’ access to housing loans without significant territorial differences. Overall, the LTV requirement for first-time home buyers could provide opportunities for wider access to the credit market without substantially increasing credit risks.

Chart 11: The evolution of new mortgage lending by LTV and contract income (left panel) and by DSTI and income (right panel)

Note: 2024 H1 data Source: MNB

3.3. The MNB will continuously monitor the adaptation to the borrower-based measures requirements and fine-tune the regulation as necessary

No significant increase has been seen in the financing of the down payment through unsecured borrowing. The share of personal loans disbursed 180 days prior to taking out a housing loan, which is likely to finance the down payment or the associated costs of home purchase, is stable at 3–4 per cent of residential mortgage lending from 2020 H2, compared to the 7–8 per cent seen in the preceding period (Chart 12). The decrease was triggered by the MNB’s executive circular issued in 2019 for institutions as a guidance for the assessment of own contributions (available in Hungarian only) and the prenatal baby support loans available from 2019.

Looking forward, customer demand for financing the down payment with uncovered personal loans may be moderated by higher LTV limits for first-time home buyers. On the other hand, the tightening of the amount of non-reimbursable state subsidies, the increase in the amount of subsidised loans available and the narrowing of the eligibility criteria for state subsidised loans could lead to an increase in the amount of housing loans and an increasing usage of the portfolio-level limit as defined in the Executive Circular, closely monitored by the MNB.

Chart 12: Estimated development of personal loans used to finance down payment

Note: The ratio of mortgage lending by contract number within the disbursement of each LTV category, for which the principal debtor took out a personal loan as well maximum 180 days before the conclusion of the mortgage contract. Without prenatal baby support loans. Source: MNB

There is no significant shift towards longer-term loans by borrowers with a high income burden. Borrowers can also adjust to high repayments by extending the maturity, which may be caused by increasing instalment payments in the recent high interest rate environment and the temporarily intensifying braking effect of the DSTI requirement. As a result of the rise in interest rates from 2022 H2, the average maturity of income-stretched housing loans with a DSTI above 40 per cent increased relative to those with a lower DSTI, with the observed maturity difference peaking at 4.5 years in 2023. In 2024, however, as the interest rate environment normalises, the spread between average maturities has also narrowed and appears to stabilise at around 3.5 years (Chart 13). However, the average maturity is not considered risky even for the 20 years typical of financially squeezed customers. No significant maturity extension was observed for consumer loans.

Chart 13: Average term according to DSTI and loan type

Note: 2024 H1 data.

From January 2025, the MNB will also support the introduction of green home loan products and increase consumer demand for green collateral and loan purposes through the green differentiation of borrower-based measures. In order to facilitate the bank financing of green real estates, the MNB decided to apply more favourable borrower-based limits for green collateral and loan purposes as of January 2025, based on the conditions of the Green Preferential Capital Requirement Program (Table 2; for a more detailed analysis of the green borrower-based requirements, see Chapter 10.):

- The LTV limit is increased from the standard 80 per cent to 90 per cent.

- The DSTI limit will be increased to 60 per cent for forint loans with an interest rate fixation period of at least 10 years, regardless of income.

Table 2: The proposed LTV and DSTI limits after the introduction of the green amendments

|

LTV limits |

||||

| Category | HUF | EUR | Other currency | |

| Mortgages | First-time buyers | 90% | 50% | 35% |

| Green collateral and loan purpose* | ||||

| Financial lease | First-time buyers | 55% | 40% | |

| Green collateral and loan purpose* | ||||

| Mortgages | Other borrowers | 80% | 50% | 35% |

| Financial lease | 85% | 55% | 40% | |

| Vehicle loans | 75% | 45% | 30% | |

Source: MNB

| DSTI limits | |||

| Category | Period of interest | ||

| Less than 5 years | At least 5 years but less than 10 years | At least 10 years or fix | |

| Net monthly income below HUF 600k | 25% | 35% | 50% |

| Net monthly income below HUF 600k in case of green loan purpose** | 25% | 35% | 60% |

| Net monthly income of HUF 600k or more | 30% | 40% | 60% |

Source: MNB

4. Basel liquidity and funding facilities

4.1. The liquidity of banks has remained ample

The LCR of the banking system is stable at around 170 per cent, with significant free buffers. After a steady increase in 2023, the sectoral LCR calculated on individual compliance stabilised at over 170 per cent in the first half of 2024 (Chart 14). Over the period covering the second half of 2023 and the first half of 2024, all banks achieved LCR levels above 140 per cent, typically with a strengthening liquidity, in line with overall liquidity, deposit and lending trends.

Chart 14: Development of institutions’ LCR

Note: The chart shows the first and ninth deciles, the first and third quartiles and the average. Excluding mortgage banks and housing savings banks, based on solo compliance data. Source: MNB

Overall, there was no change in the factors determining the evolution of the LCR and its long-term structural change. Liquid assets of the banking system increased for most of the past year, mainly due to the accumulation of liquidity deposited with the central bank and the revaluation effect of eligible collateral, mainly government bonds. The composition of the liquidity deposited with the central bank, which mainly affects liquid assets, also changed somewhat in the first half of 2024, as the simplification of the central bank’s toolkit in October 2023 allowed banks to tie up their unused funds in the central bank’s reserve account and in discount bonds. The steady increase in the LCR came to a halt in mid-2024 as cautious credit outflows began and autonomous factors affecting banking system liquidity (changes in the State Treasury Account balance, cash development) took hold. However, available liquidity remains ample. The increase in net outflows was explained by a substantial increase in deposits related to real wage growth and government bond interest payments, which was not followed by a change in inflows related to changes in lending.

The uncommitted liquidity available in the actual liquidity position is significant and developing stably. The banking system’s Operational Liquidity Reserve (OLR), supplemented by the amount of the central bank’s minimum reserve requirement, remains ample despite a slight decline. OLR averaged nearly HUF 21 thousand billion in July 2024, covering around 70 per cent of the private sector’s deposits. The increase in the liquidity reserve over the past year was explained by the liquidity-expanding effect of interest received on the high liquidity deposited with the central bank, the increase in the portfolio of eligible assets due to the revaluation effect, and the expansion in the portfolio of retail deposits, which has outpaced the growth in loans since end-September 2023, mainly seen in the retail deposit portfolio. The slight decline in the banking system’s liquidity reserve, mainly from the second quarter of 2024, was caused by the factors already referred to, which also affected the evolution of the LCR, with a reduction in liquidity on the reserve account.

4.2. Banks have an adequate funding structure and stable funding

The EU-wide NSFR requirement for long-term stable funding is met by banks with significant and growing surpluses. Banks have complied with the requirement that has a 100 per cent minimum level with a ratio of 135 per cent by the end of June 2024, up from 128 per cent last year, based on individual compliance at sector level. The sector-level stable funding surplus increased by HUF 2,800 billion, or 30 per cent, by 30 June 2024, reflecting a 9 per cent increase in the banking system’s stable funding, while required stable funding increased by only 3 per cent. The overwhelming majority of large banks had a surplus of funding above the safe buffer level of 25 percentage points (Chart 15), while small banks tended to have smaller stable funding surpluses.

Chart 15: Development of institutions’ NSFR

Note: Bottom and top deciles (vertical lines), bottom and top quartiles (light blue bars), and median values (average and median). The NSFR entered into force on 28 June 2021 (green shading), estimated data beforehand. Based on individual bank compliance data. Source: MNB

The change in the sector-level NSFR has also been favourable in terms of the internal structure of the available stable funding. Over the past year, credit growth has expanded, while the decline in liquid assets has reduced the overall moderately increasing stable funding requirements. Among stable funding, which grew more strongly and in all major item groups, liabilities arising from equity items and instruments, which can be largely traced back to extraordinary profitability, as well as in operational deposits and liabilities that cannot be identified in terms of other partners, expanded above the average. Retail and corporate funding of stable deposits grew close-to-average, showing an almost equal growth.

4.3. MNB’s supervisory requirements on LCR have increased the banks’ resilience to shocks

The MNB’s additional LCR liquidity requirements under its 2023 supervisory powers have been effective in increasing shock resilience. In the August 2023 Management Circular (available in Hungarian), the MNB informed banks of the additional supervisory requirements expected from banks in relation to the LCR, which institutions had to comply with by the end of 2023. As a result of the higher Pillar 1 MNB requirements to maintain a more stringent 140 per cent LCR, strict liquidity management, and the Pillar 2 large deposit buffer requirement, which is dependent on the deposit concentration level, both sector-level and individual LCR-levels have increased and there have been essentially no institutions below 140 per cent on a continuous basis. As a result of the Pillar 2 additional liquidity requirement, by 30 June 2024, some HUF 1,100 billion of excess liquidity emerged, with 70 per cent of individual banks having such a requirement. Typically, however, this requirement was a substantial additional requirement for smaller banks compared to total outflows. Considering the Pillar 2 surplus requirement, the overall LCR at sector level is about 17 percentage points lower. (Chart 16).

Chart 16: Sector-level LCR with the Pillar 2 requirement

Note: Sectoral averages calculated according to individual compliance. Source: MNB

5. External vulnerability mitigation instruments (FFAR, FECR, IFR)

5.1. Systemic risk associated with external vulnerabilities of the banking system is moderate

The banking system’s short external debt to total assets ratio and related external vulnerability is low by historical standards. The previous concentrated growth in the banking system’s short-term external liabilities was reversed in the past year as monetary conditions eased. However, there was no material change in the degree of vulnerability relative to total assets, as the previous increase in the portfolio also took place against a material increase in the balance sheet total. At the end of the second quarter of 2024, the domestic banking system’s outstanding short-term external debt stood at EUR 10 billion, representing 5.1 per cent of the banking system’s balance sheet total, up by 0.4 percentage point year-on-year. This is still close to the historical minimum, 2 percentage points higher, but significantly lower than the historical maximum in 2010, at 13.3 percentage points (Chart 17). Short-term external debt remains concentrated institutionally, fluctuating with intra-group transactions of the banking groups concerned, with a relatively low level of risk.

Chart 17: Development of short-term debt of the banking system

Note: Credit institutions sector, including EXIM, MFB and KELER data. Historical minimum calculated from 1998 Q1. Data for 2024 Q2 are estimated from reports of balance of payments statistics. Source: MNB

5.2. The banking system meets domestic funding requirements with adequate buffers and a secure funding structure

The elements of the macroprudential toolkit targeting the external, foreign exchange and interbank financial risks of the banking system are met by the sector with safe buffers. Banks have substantial room for manoeuvre to comply with the regulatory requirements for country-specific vulnerabilities, which are applied domestically to complement the EU-level Basel liquidity funding requirements (Chart 18). Substantial and stable buffers over time provide sufficient space to ensure safe and sustainable operations and to maintain lending capacity.

Chart 18: Compliance of the banking sector with financing requirements decreasing domestic external vulnerability

Note: Data as of 30 June 2024. The ends of the blue rectangle are the lower and upper quartiles, the ends of the dark blue line are the 10th and 90th of the distribution. Source: MNB

Banks are meeting the regulatory minimum requirement for the Foreign Exchange funding Adequacy Ratio (FFAR) in a stable manner, with a significant stable funding surplus. The sector-level indicator was at historically high levels over the past year, reaching 163 per cent at the end of June 2024. The improvement in the FFAR recently was mainly driven by an increase in the ratio of foreign currency liabilities outstanding with a remaining maturity of over one year to stable liabilities. This more than covered the increase in corporate foreign currency lending and the decrease in foreign currency deposits with no maturity and short-term household and SME foreign currency deposits, as well as non-financial corporate foreign currency deposits (Chart 19).

Chart 19: Development of asset and liability groups and financing indicators requiring and providing stable foreign currency financing

Note: Based on unweighted items of the FFAR. A temporary tightening was in effect between March and September 2020. A: assets, L: liabilities Source: MNB

The banking system’s on-balance-sheet foreign exchange surplus declined, but the sector average level of the Foreign Exchange Coverage Ratio (FECR) still remained within the allowed limits of -30 to 15 per cent, and at a safe distance from the thresholds. The foreign exchange surplus on the banking system’s on-balance sheet shrank substantially, as household and corporate foreign currency deposit holdings and non-bank corporate foreign currency liabilities declined significantly following the phasing out of interest rate caps, and foreign currency lending increased moderately. At the end of June 2024, the average FECR level in the sector was -5.5 per cent, with around HUF 3.5 thousand billion of open on-balance sheet FX positions (Chart 20). Thus, the off-balance sheet forint FX swap exposure, which was mainly required for on-balance sheet flows, has also been reduced, mitigating the excess forint liquidity. The market, counterparty and liquidity system risks associated with swap market exposures may also have fallen as the net FX swap position was also adjusted.

Chart 20: On-balance sheet open FX position and net FX swap position

Note: A negative FX swap position is a forint FX swap position. Source: MNB

The sector-wide reliance on riskier corporate funding remained stable at a low level, well below the 30 per cent maximum permitted by the interbank funding ratio (IFR) requirement. At the end of the second quarter of 2024, the sector-level average stood at 9.2 per cent, showing a slight increase compared to the same period last year. (Chart 21). Most banks, including the big ones, comply with the requirement with significant buffers. Larger branches continue to have the highest and most volatile ratios due to concentrated intra- and extra-group transactions. On the one hand, the share of funds of higher risk targeted by the IFR in corporate finance increased moderately in the past year, i.e. the share of exempted special funds with a lower risk decreased. On the other hand, within the funds counted by the IFR, the proportion of more volatile short-term exposures, including those in forint, increased, which was reflected in a smaller increase in the indicator due to higher weights. However, despite a small, unfavourable internal structural shift, the reliance on financial corporate liabilities does not show any significant vulnerability due to the relatively low level of total financial corporate funds.

Chart 21: Development of the banking system’s funds from financial corporations targeted by IFR

Note: Gross unweighted funds from financial corporations. Gross IFR represents the unweighted financial corporate funds targeted by unweighted IFR compared to the total funds. Exempted funds: mortgage-backed funds, loans received from special institutions, funds from foreign branches of credit institutions, bonds with a maturity exceeding 2 years at the time of issue, balances of margin accounts, additional capital portfolio, funds received from credit institutions belonging to the group (not from the parent company), financial derivatives within the fair balance source side value. Source: MNB

5.3. The MNB supports the operation of institutions not significant at the systemic level or those entering the market by fine-tuning the regulatory toolbox

6. Mortgage Funding Adequacy Ratio

6.1. MFAR regulation strengthens the long-term, stable funding of banks

The MFAR requirement is met by the vast majority of banks and by the sector as a whole, with significant buffers. The MFAR banking system average stood at 31.7 per cent on 30 June 2024, at almost exactly the same level as a year earlier (Chart 22). There are differences in the MFAR compliance of individual banks, but still substantial buffers are visible. Banks that are somewhat closer to the 25 per cent minimum regulatory limit can still meet the requirement securely due to the predictability of the requirement, which depends on the maturity of mortgage bonds (and the related refinancing), new issuance and the evolution of the loan portfolios, i.e. on fundamentally non-volatile balance sheet items.

Chart 22: Development of MFAR compliance

Note: The chart shows the first and ninth deciles, the first and third quartiles and the average. Source: MNB

Over the past year, we have seen a gradual increase in the total portfolio of mortgage bonds, including green mortgage bonds, and the launch of the first foreign currency issues, which has also shifted the ownership distribution in a positive direction. Growth was also supported by the MFAR regulation and the possibility of renewing mortgage bonds with the central bank. As of 31 June 2024, there were HUF 2,079 billion of Hungarian issued mortgage bonds in the market at face value, of which HUF 258 billion (12.4 per cent) were green forint mortgage bonds and HUF 198 billion (9.5 per cent) were non-green foreign currency mortgage bonds. Thus, all banks have now issued green mortgage bonds, but the issuance of foreign currency mortgage bonds has so far been limited to one bank. These changes could also strengthen ownership diversification, as the participation of domestic non-bank institutional investors in green stocks increased, while the participation of non-resident entities in foreign currency stocks also increased (Chart 23).

Chart 23: Development of the stock of domestic and green mortgage bonds in circulation according to ownership sectors

Note: Data at face value. Source: MNB

Under the current, unfavourable market conditions, given the significant maturing mortgage bond stocks and the gradual recovery of the mortgage loan portfolio, maintaining MFAR compliance may be challenging for some institutions in the period ahead. In the remainder of 2024, HUF 305 billion of mortgage bonds, representing 15 per cent of the total stock, and in 2025, HUF 269 billion of mortgage bonds, representing 13 per cent of the total stock, will mature, creating a substantial issuance need (Chart 24). In 2024 and 2025, taking into account the estimated growth of mortgage loan portfolios, a minimum issuance of around HUF 420 billion may be essential to maintain MFAR compliance for issues without green rating and a minimum issuance of around HUF 280 billion for green issues. If the aim is to maintain the current level of MFAR buffers, issuance of HUF 789 billion or HUF 526 billion may be required, depending on whether green or non-green mortgage bonds are issued.

Chart 24: Issuance needs of mortgage banks in 2024-2025

Note: Estimate based on MFAR compliance data as of 30 June 2024. Taking into account the predicted increase in loan portfolios in the denominator of MFAR. In the case of the issuance need, adaptation needs emerging at other banks through refinancing relationships also appear. Source: MNB

6.2. The MNB has eased its regulation in the light of changed financial market conditions

As the momentum and fundamentals of mortgage bond market developments are not currently favourable, a wait-and-see approach to further regulatory tightening is justified, and even a postponement of previously planned tightening was necessary. Given the current uncertainties, expected returns remain high, albeit moderately declining (Chart 25). This will keep mortgage-based funds more expensive compared to other available funds, such as retail deposits. In addition, the build-up of the corresponding credit portfolio, mainly green, will only start gradually. For these reasons, the MNB may decide on the potential timing of the previously planned MFAR tightening in the future, depending on the normalisation of the economic and financial market environment.

Chart 25: 3- and 5-year domestic mortgage bond and government bond market yields

Note: BMBX: mortgage bond market index; 3Y, 5Y: 3 and 5 year terms. Source: MNB

Green issuance can meet the regulatory requirement at a lower cost, but its main limitation, and in particular the limitation of issuance in the quantity required for foreign currency mortgage bonds, is the lack of sufficient free green collateral and the slow pace of its build-up. Following a significant drop in the lending activity in 2023, mortgage lending is currently showing a substantial pick-up. At the same time, the amount of green loan assets already built up and not yet encumbered remains limited, preventing the issuance of large series of green mortgage bonds. Thus, for all banking groups, and in particular for a potential large volume of green foreign currency mortgage bond issuance, there are significant challenges in accumulating the necessary loan portfolio with sufficiently high energy efficiency backing for green mortgage bond issuance. We estimate that around HUF 180 billion of green mortgages could be available for further green issuance, with different proportions available per bank. As the green mortgage bonds, typically issued in 2021–2022, are not expected to mature in the near future, this way there is no ”released” collateral either. Another obstacle remains the lack of availability of energy data on the collateralisation of existing loan portfolios by banks.

The MNB has postponed for an indefinite period the green requirement for new foreign currency mortgage-backed liabilities eligible for the MFAR since 2022, which was previously postponed by one year and will enter into force on 1 October 2024. In view of the uncertain conditions in the mortgage bond market, the administrative difficulties and time requirement for foreign currency issuance, the large stock of maturing and renewable mortgage bonds, and the challenges of building up green collateral in sufficient volumes, the MNB considered the postponement justified. The investor diversification that comes with an increase in foreign currency issuance can bring significant financial stability benefits in terms of stable funding, which can only be leveraged, given these constraints, by postponing the green requirement under the current market conditions.

7. Capital buffers of systematically important institutions (OSII-B)

The 2024 Annual Periodic Review of the MNB classified again the same seven banks as in previous years to be domestic (Other Systemically Important Institutions – O-SIIs). Systemically important banks have to comply with the individual buffer rate target levels from 2024 on, this concludes the gradual rebuilding of the buffers following the release introduced at the start of the coronavirus pandemic has come to an end. The relatively modest change in the systemic importance and concentration of O-SII banks in the past year, mainly due to the foreign acquisitions of OTP Bank Plc, did not justify any change in buffer rates.

Under the identification process for 2024, the same seven groups of banks as last year had been classified as other systemically important credit institutions. During the latest regular identification of Other Systemically Important Institutions (O-SIIs) headquartered in Hungary in 2024, the MNB continued to use the same measurement of systemic importance as in previous years, based on the aggregation of the EU-harmonised core indicators and the added optional domestic indicators. Using the audited data as of 31 December 2022, the MNB thus reviewed the O-SII scores representing systemic importance, which, as in previous years, exceeded the 275 basis point threshold for systemic importance for seven banking groups (Chart 26).

Chart 26: Components of the scores of other systemically important institutions and their final buffer rates

Note: The scores shown are the results of the 2023 review. The horizontal blue line indicates the standard 350 basis points in the EBA Guidelines, while the red line indicates the domestic threshold level above which a bank can be rated O-SII, reduced to 275 basis points in 2020 as permitted by the EBA Guidelines. Source: MNB

Given the stability of the scores and market concentration of O-SII banks and their adequate capital position, the two-year gradual re-introduction of buffers has reached the targets by 2024. As in previous years, the distribution of scores measuring systemic importance does not show a significant shift and has proved to be stable (Chart 27). The overall market concentration of major banks continued to increase slightly compared to previous years (8,087 basis points). The more stable components of the scores, primarily size-related balance sheet totals and real economy loans outstanding, expanded significantly during 2022, which year forms the basis of the 2024 identification exercise, with an average yearly growth rate of over 10 per cent for O-SII banks. This increase was relatively steady and did not significantly restructure the relative position of the banks concerned. Of OTP Group’s acquisitions, only the Albanian one was completed in 2022, with the larger Slovenian and Uzbek expansions expected to show up in the systemic importance scores in 2024, while the sale of the Romanian subsidiary will only have a longer-term impact. In comparison with the more stable components, the more volatile financial market and interbank indicators often cause only temporary variance in scores. Still, a shift with structural characteristics in terms of the indicator of outstanding debt securities continued, with the issuance of bonds required to comply with MREL requirements. Relative positions have become more balanced as more O-SII banks made large issuances. O-SII buffer compliance required banks to hold a HUF 627 billion of capital at the end of 2024 Q1, while operating with a substantial voluntary capital buffer of nearly HUF 1,856 billion, although there are significant individual differences. important-SII banks continued to operate with high voluntary capital buffers of HUF 1,873 billion at the end of 2024 Q2 (see Chart 5 at the banking system level). Individual voluntary buffer ratios typically improved or remained at favourable levels compared to the same period of the previous year. The O-SII buffers, which have reached their final value by 2024, required around HUF 639 billion of capital at the same time. Overall, the stable capital positions and profitability will continue to provide the opportunity to maintain lending capacity.

Chart 27: Changes in the scores of other systemically important banks

Note: The years indicate the validity period of the scores, the scores are calculated by the MNB on the basis of the audited data provided by December 31 of the antepenultimate year. Source: MNB

Macro-prudential monitoring also follows closely the systemic risk contribution of systemically small but rapidly expanding medium-sized banks. The banking system stress experienced in the US in the spring of 2023, triggered by medium-sized US credit institutions, has again highlighted that smaller institutions can trigger a confidence crisis, financial information contagion and may require the intervention of monetary, deposit insurance and prudential authorities, even though their systemic footprint falls short of the impact of the largest systemically significant players.1 In particular, institutions that operate with similar business and funding models and portfolio segmentation (e.g. US commercial real estate lenders) may be affected. In the Hungarian market, the annual growth rate of significance scores among banks other than institutions identified as O-SIIs has shown a noticeable and concentrated increase in recent years. The concentrated expansion was reflected in indicators describing both payments, deposits and interconnectedness, as specialised service provision increased in some systemically important activities, for example through the development of digital channels or as the partner institution of specialised state credit institutions (Table 3). Interconnectedness with non-bank financial institutions is also expanding through their expansion with subsidiaries. Although the significance of these banks remains limited and their score is still considerably below the country-specific, tightened 275 basis points O-SII identification threshold, nonetheless the MNB monitors their increasing contribution to systemic risk from a macroprudential perspective.

Table 3: Some indicative indicators of the expanding activities and specialised business models of the domestic credit institutions that do not qualify as O-SII

| Domestic real economy loans / deposits score at non-O-SII banks (2024Q2) | 447 bp / 509 bp |

| Increase in total assets / deposit market share for non-O-SII banks (2023-24Q2) | 5,1% / 4,1% |

| Proportion of new accounts opened digitally at non-O-SII banks compared to O-SII banks (2023-24Q2) | 54% |

| Proportion of transactions initiated by real economy customers via remote payment channels (2024Q1-Q2) | 94% |

| Increase in the proportion of cards registered to mobile wallets at O-SII and non-O-SII banks (2022Q4-2024Q1) | 36% / 102% |

| Increase in the number of younger customers (under 35) with bank accounts at O-SII and non-O-SII banks (2022-2023) | 11% / 25% |

Note: Credit institution branches operating on the domestic market are not included in the non-O-SII domestically based credit institutions

8. Systemic Risk Buffer (SyRB)

8.1. Project loan exposures financing commercial real estate are exposed to increasing risks

The commercial real estate market still shows low but increasing cyclical and structural risks. In the commercial real estate market, vacancy rates have risen substantially for both Budapest office and industrial/logistics properties, but are still not historically high, while further increases are expected (see more in Commercial Real Estate Market Report). At the same time, investment turnover in 2023 was 38 per cent down on the previous year, and capital values in the Budapest office market fell by 9 per cent in one year, reflecting the rise in prime yields. The rising commercial real estate market risks are mitigated by the credit institutions’ moderate exposure through project loans and the adequate portfolio quality of the project loan portfolio (Chart 28). Looking ahead, however, risks may increase substantially as a result of the still uncertain macroeconomic outlook, new supply coming to the market in the near future, and structural changes in the commercial real estate market (e.g. the escalation of online shopping and the demand for flexible office leases, ”rightsizing“, the focus on sustainability in the decisions of both tenants and investors).

Chart 28: The evolution of outstanding commercial real estate project loans

Note: Data before June 2023 based on L70 reporting, relating to domestic and foreign exposures, while after June 2023 based on transaction level data according to HITREG. Therefore, the different periods can only be compared to a limited extent due to modifications affecting data content and calibration. The ratio of a bad portfolio is the ratio of the bad portfolio to the total portfolio. Source: MNB

8.2. Several banks have revised their project loan exposures in response to the reactivation of the systemic risk buffer

In view of the risks also visible in the global commercial real estate market, in June 2023 the MNB decided on the reactivation of the Systemic Risk Buffer (SyRB) for preventive purposes, which was suspended in the wake of the coronavirus outbreak. Prior to the coronavirus outbreak the Bank successfully used the facility to support the off-balance sheet clean-up of problematic commercial real estate project loans concentrated in the balance sheets of large banks and to strengthen the shock resilience of banks against the remaining exposures. The reactivation of the tool suspended during the pandemic was justified as the pandemic subsided, along with the revitalisation of commercial real estate lending, the still low but increasing risks in the global commercial real estate market, and the risk predictions and calls for action of international organisations (e.g. the European Systemic Risk Board).

By reactivating the SyRB, the MNB is strengthening the shock resilience of banks against commercial real estate market risks. The introduction of SyRB in the current low-risk period will, on a preventive basis, strengthen the resilience of banks to shocks and encourage timely portfolio adjustments. Accordingly, the MNB announced in October 2023 the revised criteria for the establishment of the SyRB, thus providing banks with sufficient adjustment time, as the institution-specific SyRB ratios were set on the basis of the methodology known to banks.

Based on the commercial real estate financing project loan portfolio and the capital position as at 31 March 2024, the MNB determined the capital buffer requirements for each institution. In line with the low risk levels and the inherently preventive nature and repeated application of the tool, none of the banks were required to have an effective SyRB from 1 July 2024. The next review of the capital buffer rates will be carried out by the MNB within one year, by June 2025, based on data as of 31 March 2025, in addition to the continuous monitoring of exposures.

The announcement of the reactivation of the SyRB in June 2023 has effectively stimulated a prudential review of project loan portfolios of banks for commercial real estates. As a result of the announcement and discussions with banks, the restructured portfolios of several banks that had increased due to participation in the payment moratorium during the COVID-19 pandemic have been reviewed and treated in line with prudential requirements, as well as reclassified back to performing category as necessary (Chart 29).

Chart 29: The change in SyRB calibration indicator due to the adaptation of banks

Note: The calibration indicator is the weighted stock of the targeted project loan stock (the numerator of the calibration indicator) and the quotient of the Pillar I capital requirement (the denominator of the calibration indicator). Source: MNB

8.3. The SYRB is mainly currently targeting residential property risks across the EU, but could also be used to mitigate climate risks

9. The MNB’s resolution activity

9.1. Compliance with the MREL requirement mandatory from 1 January 2024 has been achieved by the institutions concerned

On 1 January 2024, the institutions met the mandatory MREL requirements set by the MNB. The institutions concerned were required to fully comply with the MREL requirements set out in the resolution planning, essentially after three years of adjustment along a linear path, from 1 January 2024. The requirements in terms of total risk-weighted assets, excluding capital buffer requirements, range from 18.9 to 28.6 per cent.

Most of the adjustment took place in 2023 Q4, mainly through foreign issuance. After the intermediate targets were met, several of the institutions concerned took a “wait-and-see” position, which meant that the full MREL-eligible resources of around HUF 600 billion essential for meeting the final requirement in 2023 were raised in 2023 H2. The vast majority of these were issues to foreign institutional investors, parent bank loans and bond purchases. The volume of domestic retail borrowing and domestic institutional purchases were much lower.

The institutions concerned have met this requirement by mobilising several types of MREL-eligible resources. Institutions have adapted by issuing various capital instruments and by issuing MREL-eligible bonds – senior and senior non-preferred (external MREL) bonds. In addition, banks with a centralised resolution strategy (SPE) through parent bank intervention also met the requirements by providing a parent bank loan that enables the flow of losses to the parent bank, or by issuing MREL-eligible bonds subscribed by the parent bank (internal MREL) for the implementation of the strategy. (Chart 30) The pricing of MREL-eligible liabilities was largely determined by their seniority, with equity-type liabilities being more expensive, while non-priority unsecured bonds and senior bonds and parent bank liabilities were cheaper.

Chart 30: MREL capacity’s distribution for large banks

Source: MNB

Of the external MREL-eligible funds mobilised, HUF 275 billion will – ceteris paribus – mature in the next two years. The easing of financial markets in 2023 H2 and 2024 H1 and the declining yield environment provided a favourable opportunity to renew external MREL-eligible resources. At present, we see that emissions are significantly oversubscribed. (Chart 31)

Chart 31: Expiry of external MREL eligible liabilities

Source: MNB

Core Tier 1 capital held to meet capital buffers is from 2023 no longer regarded as an MREL-compliant resource because of the prohibition on using it concurrently for several purposes. In the calculation of the MREL requirement, capital buffers were excluded from the calculation, while the core Tier 1 capital (CET1) that covers capital buffers is not part of MREL-compliant funds. Consequently, a possible increase in buffers will reduce the stock of available MREL-eligible resources and may therefore result in need for issuance. The activation of the countercyclical capital buffer for domestic exposures of 0.5 percentage point on 1 July 2024 could lead to an increase in MREL requirements of around HUF 112 billion for the institutions concerned, based on data at the end of 2024 Q2, excluding the impact of changes in exposures in the estimate. The increase of the countercyclical capital buffer to 1 per cent in July 2025 could also increase this by another HUF 112 billion.

9.2. MREL compliance is continuously monitored by the MNB, while another significant improvement of the methodology supporting resolution planning started in 2023

10. The MNB’s consumer protection activities

10.1. The number of credit institution customers requesting MNB action increased again in 2023

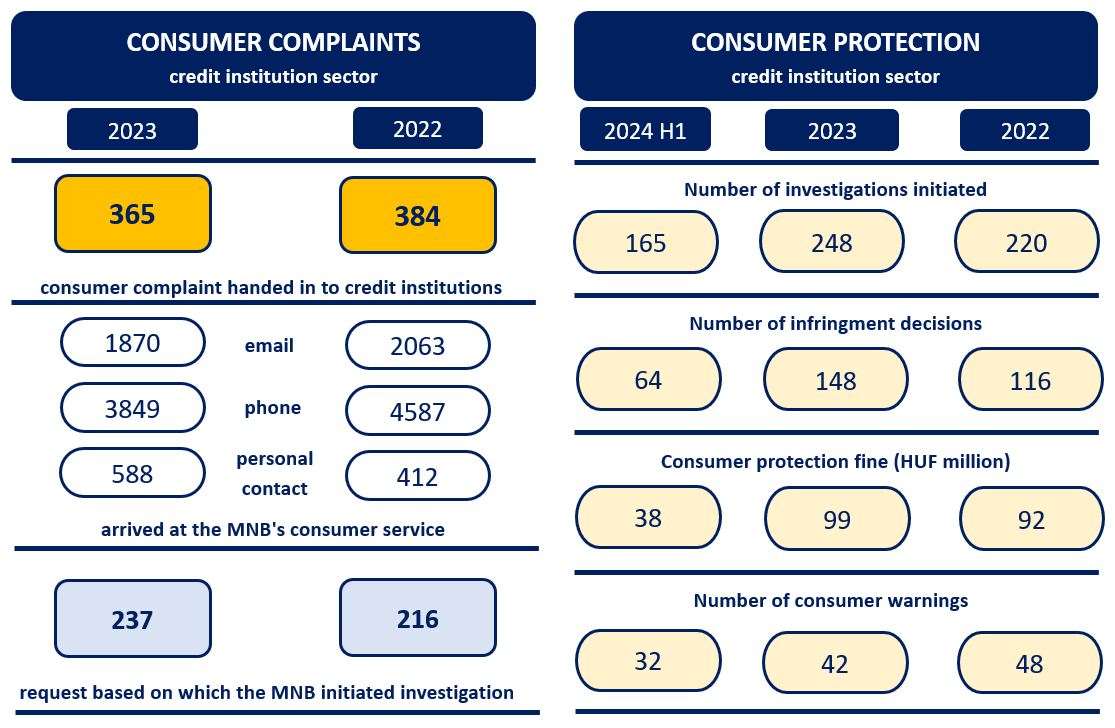

Despite a decrease in the number of complaints to the credit institution sector, the number of consumer complaints to the MNB continued to increase in 2023. In 2023, the number of complaints filed with credit institutions decreased by 5 per cent, while the number of consumer complaints filed with the MNB increased by 10 per cent in 2023, similar to the previous year (Chart 32). The majority of consumers continued to complain about the institutions’ handling of complaints and their handling of fraudulent online or phone transactions. While the number of investigations launched by the MNB has increased, the share of decisions finding non-compliance has decreased (below 60 per cent in 2024 H1). The consumer protection warnings issued as part of the continuous monitoring, which allow for rapid action, were typically issued in 2023 due to shortcomings in the information published by the institutions. The most common subjects of complaints received by credit institutions in 2023 were, in order, financial abuse, settlement disputes and the execution of orders. Although credit institutions received fewer complaints, the share of complaints on financial abuse increased by nearly 5 percentage points to 27.3 per cent in 2023.

Chart 32: Consumer complaints and consumer protection activities in the credit institution sector

Source: MNB

10.2. The MNB has drawn attention to shortcomings in institutional practices related to handling overdue loans

10.3. MNB found minor information gaps in online personal loan applications

10.4. The MNB has taken further steps to curb cyberfraud by issuing executive circulars to domestic payment industry operators

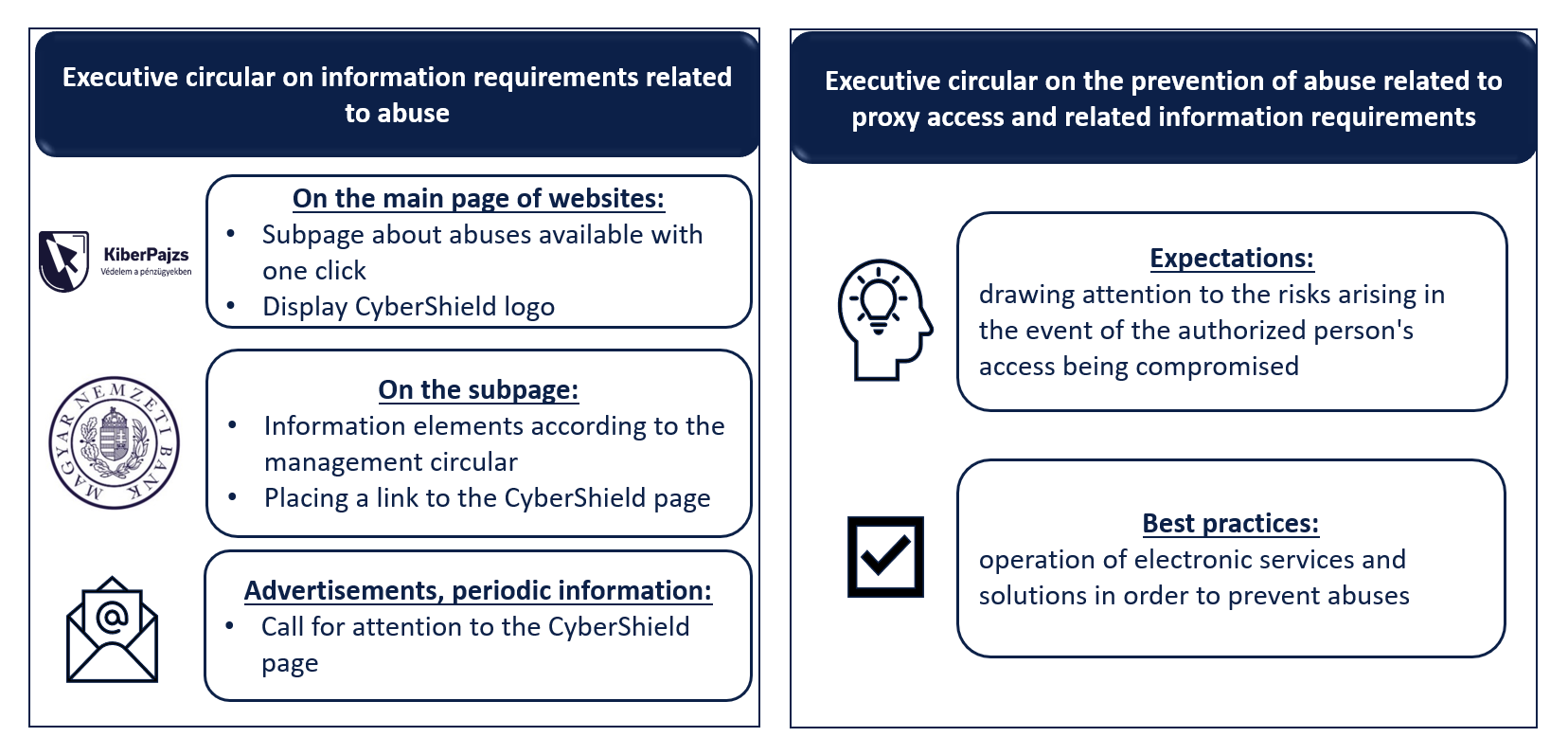

Cyber fraudsters continue to actively attack customers in a variety of ways. The MNB has therefore continued to be actively involved in the CyberShield cooperation during the reference period and issued two executive circulars (Chart 33) in 2024 H1 to curb cyberfraud.

The aim of the executive circular on information expectations in relation to payment service abuse is to help the relevant payment service providers to ensure that their websites comply with the expectations set out in the MNB Recommendation on the prevention, detection and treatment of payment service abuse, aimed at educating and informing customers, in a uniform and attention-grabbing manner. The MNB requires, among other things, that market players should present to consumers on their websites (by navigating from the main page of the website) a separate information page on the main types of fraud, the steps to avoid and prevent them, and who and how to contact at the financial institution in question if they detect abuse. The circular also requires payment service providers to draw attention to the kiberpajzs.hu (cybershield) website in their customer information leaflets on bank accounts and bank cards.

In another circular the MNB called on account management institutions to warn their customers of the risk of cyberfraud by 15 May 2024 for those with existing authorisations and for those granting new authorisations, as criminals can (also) gain access to the accounts of authorised customers by compromising their internet or mobile banking access. In the MNB’s view, it is a good practice for service providers not to set the default proxy settings for certain channels (e.g. online banking), but for authorisers to decide on their own via which channels they allow access to their accounts, and if this can be changed (even by setting transaction limits) later. It is also a good practice if the abuse-filtering systems of institutions take into account authorising party-authorised party relationships.

Chart 33: Expectations of MNB circulars aimed at curbing cyber fraud

Source: MNB

BOX 2: The potential financial stability and consumer protection risks related to the growth of deferred payment schemes

11. Financial stability risks of climate risk and options for their macroprudential management

11.1. The MNB is closely monitoring the financial systemic risks of climate change

Sectoral credit exposures in the banking system’s corporate loan portfolio, which are vulnerable to migration risks, are at high levels and have expanded. In recent years, the so-called climate policy relevant sectors (CPRS), used recurrently by risk monitoring systems, have increased at a similar pace as the growth of the overall corporate loan portfolio Alessi and Battiston (2022)) (Chart 34). The ratio of the CPRS credit exposure to the banking system’s total corporate portfolio has not changed significantly since 2019 from its relatively high level of around 56 per cent at the end of 2024 H1. This measurement approach provides an upper estimate of the climate vulnerable exposures of selected sectors 2, which can be reduced by, for example the EU 2020/852 Taxonomy Regulation and its complementary EU 2021/2139 regulation or other sustainable financing schemes, but even beyond this there may be significant disparity in the climate change-related financial risks of activities in the covered sectors. There are significant differences between the portfolio composition of credit institutions in terms of the share of CPRS exposures and the GHG intensity of the activity financed. Including corporate credit and securities exposures in the calculation, the risk level of the portfolios is assessed at an institutional level by the banking system climate risk matrix of the MNB Green Financial Report (for the methodology see Ritter (2022)). Based on the updated values of the matrix for 2024 Q2, four domestic systemically important banks have a relatively higher risk rating (the so-called middle-top quartile of the matrix), while another three have a more moderate risk rating (the so-called middle-bottom quartile).

Chart 34: The evolution of exposures to climate policy relevant sectors (CPRS)

Note: The graph shows end of the year loan exposures (outstanding principal debt) in case it is not specified further. For the NACE sectoral definition of the CPRS classification, see Alessi and Battiston (2022), Battiston et al. (2022) and Battiston et al. (2017). The green loan part of the exposure to the CPRS sectors includes i) the EU green taxonomy aligned exposure as they are provided in the credit register data reporting, ii) the green corporate loans of the preferential capital requirements program, iii) green loans provided under the Gábor Baross Reindustrialisation Loan Program and iv) loans benefiting from the CRR Art. 501.a infrastructure supporting factor. Green loans financing fossil fuel, energy intensive, transport and agriculture CPRS sectors are not shown on the graph as their order of magnitude is yet too small compared to the scale of the graph. Source: MNB

The climate change risk intensity of the vulnerable elements of the loan portfolio also increased. In order to map climate change-related financial systemic risks, the MNB expands the scope of examined risk indicators every year, in parallel with the risk indicators of EU surveys (for the latest European overview, see the ECB/ESRB (2023) report). A measure of climate risk exposure, which is also representative of the intensity of the risks, is shown by the increase in credit exposures weighted by the annual share of GHG emissions from the industries (Chart 35), of which around two-thirds have a longer term to maturity. These transactions could still be affected by the possible intensification of transition risks in the medium term. The reallocation of lending between industries towards high output sectors was moderate, with the increase in the indicator mainly due to a growth in the loan portfolio. However, the so-called GHG real financing gap indicator (cf. the similar carbon-financing tilt indicator) nuances the changes further, ECB/ESRB (2023)), which is the ratio of GHG emissions weighted by loan financing to the same emissions weighted by the sectoral gross value added (GVA) to compare the GHG intensity of sectoral GVA to that of the sectoral loan financing, and indicate whether loan financing diverges towards sectors with relatively higher or lower GHG intensity. The evolution of the indicator is driven by high value-added (GVA) activities requiring less and less GHG emissions, while the change in the composition of activities financed by the banking system’s loan portfolio is at any rate smaller, i.e. activities with relatively higher GHG emissions receive a larger share of the banks’ loan portfolio than their share of real economic value added. It is also worth observing the evolution of the Bank Carbon Risk Index (BCRI), which is regularly updated in the MNB’s Green Finance Report, and shows that after a stagnation and slow decline in transition climate risks between 2020 and 2022, a sharp increase in exposure was noted in the Hungarian corporate loan portfolio in 2023 (for the methodology see Bokor (2021)). The BCRI is adjusted for more accurate risk characterisation by including green corporate loans, which are considered climate risk-free and whose domestic portfolio exceeded HUF 633 billion at the end of 2024 Q2, and by including individual GHG emissions of companies participating in the European Emissions Trading System (ETS) for sectoral GHG intensity data (Ritter (2023)).

Chart 35: GHG emission weighted loan exposures related to transition risks

Note: The graph uses end of the year loan exposure (outstanding principal debt) data and the greenhouse gas emission (GHG) data of the given year. For the weighted loan exposures, the GHG emission weights are given by the sectoral shares in proportion to the total industrial GHG emissions. The GHG real financing deviation indicator (carbon tilt measure, CTM) is the ratio of GHG emissions weighted by the share of loan exposures in total corporate loan exposure and the GHG emissions weighted by the sectoral gross added value (GVA), that is,  where index i denotes the economic sectors, Loani the loan financing of sector i, GHGi the emission of pollutants and GVAi the added value of the product. Source: Eurostat, MNB

where index i denotes the economic sectors, Loani the loan financing of sector i, GHGi the emission of pollutants and GVAi the added value of the product. Source: Eurostat, MNB

11.2. The MNB supports the achievement of climate change targets through green differentiation of borrower-based measures within its macroprudential policy as well

Since 2021, no significant improvement in the energy efficiency of mortgage-financed properties is visible, with the exception of properties financed under the Green Home Programme (GHP). The share of better-than-modern collateral in new residential mortgage lending has been low and stable since 2021 (rated BB or better under the ratings in effect until October 2023 and A or better under the ratings currently in effect), ranging from 10 to 20 per cent, with the share temporarily approaching 50 per cent during the Green Home Programme’s subsidy period (Chart 36). Based on this, there is considerable room for strengthening the contribution of mortgage lending to energy efficiency improvements.

Chart 36: Housing loan disbursement by the energy performance of funded residential real estates

Note: Taking into account the new energy classifications applicable from November 2023. Missing data are explained by potentially unavailable Energy Performance Certificate data at the time of the home purchase, along with data quality reasons. The MNB continuously strives to minimise the proportion of missing data. Source: MNB

Modern real estates are concentrated around low-risk borrowers with above-average incomes. Energy-efficient, modern properties have a significant price premium compared to less modern ones, making them mainly available to borrowers with an above-average income. While among borrowers with an average net income of less than HUF 400,000, the share of modern real estates was more than 3 per cent in the period under review, it reached almost 20 per cent for loans disbursed to borrowers with a net income of more than HUF 1 million between 2021 and 2024 Q2.

Higher energy-efficient properties can be attained with higher down payment and a stronger income stretch. Loans financing properties with unfavourable energy characteristics show an increased LTV-stretch, which may indicate that borrowers with insufficient down payment are less likely to have access to modern properties compared to borrowers with higher savings. In addition, loans financing energy-efficient properties show an increased strain on borrowers’ incomes, which may confirm that borrowers who are able to provide higher down payment and who have access to the loan required for purchasing green properties have a stronger income squeeze due to their higher loan amounts (Chart 37).

Chart 37: The distribution of housing loan disbursement by energy performance and LTV and DSTI values

Note: Distribution by volume. Only housing loans for constructions or purchase, without Green Home Programme loans. Taking into account the new energy classifications of November 2023. Source: MNB